Short Term Rental Insurance: A San Diego Owner’s Guide to Smarter Coverage

- Mark Palmiere

- Oct 10, 2025

- 14 min read

Updated: Nov 28, 2025

TL;DR: Key Takeaways on Short Term Rental Insurance

Standard Homeowner's Insurance is Not Enough: Your personal policy likely has a "business exclusion" clause, leaving you financially exposed the moment you accept paying guests.

Three Pillars of Coverage: A solid short-term rental insurance policy must include Liability, Property & Contents, and Loss of Income coverage to fully protect your investment.

Platform Protection (AirCover/VRBO) Has Gaps: These are guarantee programs, not legal insurance contracts. They offer limited protection and leave significant gaps that a private policy covers.

Assess Your Unique Risks: Your policy needs to match your property. A San Diego beacinh house with a pool has different risks than a downtown condo.

Expert Management is Key: Partnering with a professional manager like West Coast HomeStays ensures you have the right insurance and a strategy to maximize revenue and minimize risk.

Think of short-term rental insurance as a business-grade policy built specifically for the risks that come with hosting paying guests. We're talking about things like property damage, liability claims if someone gets hurt, and even lost income if your rental is out of commission.

Your standard homeowner's policy just wasn't designed to cover these kinds of commercial activities. That's why having specialized insurance isn't just a good idea—it's essential for protecting your investment and achieving the kind of hands-off success that partners like West Coast HomeStays deliver for San Diego owners.

Your Quick Guide to San Diego STR Insurance

For anyone owning property in San Diego, getting your insurance right is the bedrock of a successful rental business. It's what protects your valuable asset from all the "what ifs." This is one of those areas where partnering with a savvy local host makes a world of difference. We don't just focus on maximizing your income; we make sure your investment is properly shielded from day one.

Consider it your commercial safety net. With the right policy in place, you can stop worrying and focus on returns. Without it, a single unexpected incident—a guest slipping by the pool or causing accidental damage—could spiral into a financial nightmare.

Why Standard Home Insurance Just Won't Cut It

It's a common mistake. Many owners assume their homeowner's policy has them covered, but that's rarely the case. Most personal policies contain a "business exclusion" clause. The moment you accept money for a stay, you're running a business, and that clause can void your coverage entirely.

This leaves you exposed to some serious risks.

Homeowner's Policy vs STR Insurance Coverage

Take a look at this table. It breaks down the critical gaps a standard policy leaves open and how specialized short-term rental insurance steps in to fill them.

Risk Category | Standard Homeowner's Insurance | Short Term Rental Insurance |

|---|---|---|

Guest Injuries | Typically Excluded (Business Activity) | Covered |

Guest-Caused Damage | Often Denied | Covered |

Loss of Rental Income | Not Included | Covered |

Theft by Guests | Generally Not Covered | Covered |

The difference is night and day. What a homeowner's policy sees as a deal-breaker (commercial activity), an STR policy is built to handle.

Protecting Your San Diego Investment

Figuring out the ins and outs of short term rental insurance doesn't have to be a headache. The right coverage is a foundational piece of your rental strategy, protecting you from liability while preserving your property's value. Understanding these key differences is the first step. For a much deeper dive into running a successful rental, check out our comprehensive guide to short-term rental management in San Diego.

A solid policy gives you the confidence to host guests, knowing your asset is protected and can continue generating income no matter what. For any serious investor in San Diego’s booming vacation rental market, it's completely non-negotiable.

Why Your Homeowner's Policy Falls Short

So many San Diego property owners make the same critical mistake: they assume their standard homeowner's insurance policy is enough to cover their rental. It’s an easy assumption to make, but it’s one of the most expensive errors a host can run into.

Relying on your homeowner's policy for a short-term rental is like using your personal car insurance to cover a full-time pizza delivery business. The moment money changes hands for a service, the rules of the game change entirely.

Once you accept payment from a guest, you’re not just a homeowner anymore—you’re running a commercial business. Your personal policy was never designed for that, and it almost certainly contains a "business exclusion" clause that will leave you high and dry when you need it most.

The Business Exclusion Clause Explained

Think of the business exclusion clause as a very clear line in the sand. Your personal policy is there to protect you, the resident, from the normal risks of owning a home. But when you start inviting paying guests, you introduce a whole new set of commercial risks that your insurer never agreed to cover.

Your insurance company sees your vacation rental less like a home and more like a hotel. The risks are different, the liabilities are higher, and a personal policy just isn't built—or priced—to handle that.

If a guest gets hurt or something goes wrong during their stay, your insurance provider has every right to point to that clause and deny your claim. That leaves you on the hook personally for all the damages, medical bills, and legal fees.

Real-World Scenarios Where You Are Exposed

It’s easy to dismiss this as technical jargon until you see how it plays out in the real world. Thinking "it won't happen to me" is a huge gamble. Proper short term rental insurance is specifically designed for these situations, while a homeowner's policy would leave you completely vulnerable.

Here are a few all-too-common scenarios where your standard policy would almost certainly fail you:

A Guest Slips by the Pool: A family is loving your Pacific Beach property, but one of them slips on a wet spot near the pool and suffers a serious injury. Their medical bills and the lawsuit that follows could easily climb into six figures. Your homeowner's policy will likely deny the claim, citing the business exclusion.

Theft During a Stay: A guest calls in a panic, claiming their expensive laptop and jewelry were stolen from the property. They blame you for inadequate security. A standard policy almost never covers the theft of a paying guest's property.

Major Renter Damage: A group of guests throws an unauthorized party, leaving you with thousands of dollars in damage to your furniture, walls, and floors. Because the damage happened during a paid, commercial activity, your claim will probably be rejected.

The True Cost of Inadequate Coverage

Without dedicated short term rental insurance, you are effectively self-insuring against every possible disaster. A single major incident could not only wipe out your rental income for years but could also put your entire property at risk.

This is exactly why savvy investors and professional property managers see specialized insurance not as just another expense, but as a non-negotiable cost of doing business right.

Navigating the world of insurance is a critical part of running a successful rental. A professional partner like West Coast HomeStays knows the San Diego market inside and out, including the specific protections you need to keep your investment safe. Making sure you have the right coverage isn't just a box to check—it's a core part of our management philosophy, giving you the ultimate peace of mind.

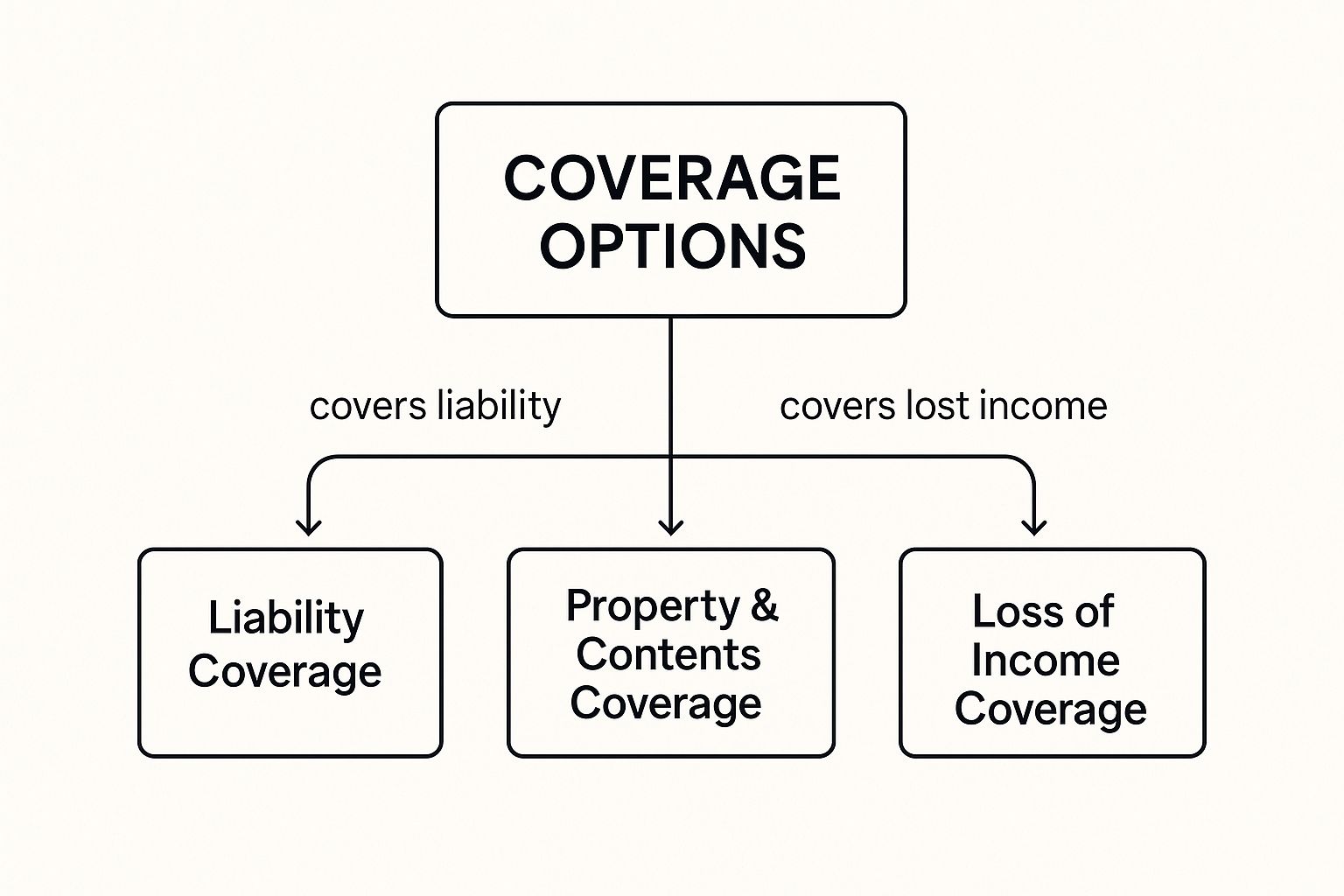

Understanding Your Coverage Options

Trying to get your head around short term rental insurance can feel a bit overwhelming, but it really just comes down to three core layers of protection. Your standard homeowner's policy won't cut it here; this is specialized insurance built for the business side of renting your property. Think of each coverage type as a different part of a security system, all working together to protect your San Diego investment.

This map breaks down the three essential pillars that make up a solid STR insurance policy.

This visual shows how liability, property and contents, and loss of income coverage create a safety net for your business. Getting a handle on these three is the first step toward getting some real peace of mind.

Liability Coverage: The Foundation of Your Protection

Liability coverage is, without a doubt, the most critical piece of your policy. It’s your financial shield if a guest gets hurt on your property and decides to sue.

Imagine a guest slips on a wet tile by the pool at your La Jolla rental and ends up needing surgery. This is exactly what liability coverage is for—it's designed to handle their medical bills and your legal defense costs. A single accident like that could otherwise put your entire investment at risk.

A good policy will offer at least $1 million in liability protection, which is becoming a standard requirement in many cities anyway. This coverage kicks in for guest injuries, damage to their property, and other third-party claims. It’s your best defense against the unpredictable things that can happen when you're a host.

Property and Contents Coverage: Guarding Your Physical Assets

While liability insurance protects you from lawsuits, property and contents coverage protects the actual building and everything you've put inside it. This is what covers your house, furniture, appliances, and decor from damage caused by guests, or from other events like a fire or theft.

Just think about the wear and tear a busy summer season can put on your Oceanside beach house. This coverage helps pay for repairs or replacements when a guest accidentally breaks an expensive appliance, damages that custom sofa, or causes other significant cosmetic damage.

It's not just about major disasters. Comprehensive contents coverage is about protecting the specific, high-value items that make your San Diego rental a top-tier destination—from the smart TVs and quality linens to the fancy kitchenware.

This part of your policy ensures you can get your property back to its five-star condition quickly without having to pay for everything out of your own pocket.

Loss of Income Coverage: Protecting Your Revenue Stream

What happens if a fire or major water damage makes your property unrentable for a few months? You’re not just looking at repair costs—you’re also losing thousands in rental income. This is where loss of income coverage, sometimes called business interruption insurance, is a lifesaver.

This protection pays you back for the rental income you would have made while your property is being repaired after a covered event. It gives you the cash flow to keep paying your mortgage, taxes, and other bills, stopping a temporary problem from becoming a long-term financial disaster.

For a popular San Diego property, losing three months of peak-season income could be devastating. This coverage keeps your business financially stable, even when your doors are temporarily shut. Understanding its role is key, especially if you're exploring different rental strategies. To see how it fits into other models, check out our guide on how mid-term rentals fit into insurance and housing needs.

Platform Protection vs Private Insurance

If you're new to hosting, it’s incredibly easy to see something like Airbnb’s AirCover or VRBO’s Host Guarantee and assume you’re all set. But that’s a dangerous assumption. While these platform protections are a decent first line of defense, they were never meant to replace a real short term rental insurance policy.

Here’s a simple way to think about it: a platform guarantee is like getting store credit for a returned item. It’s helpful, but you can only use it in one place under their rules. A private insurance policy is like cash in your pocket—it’s a binding legal contract that gives you specific, enforceable rights and far more flexibility.

Understanding the Critical Gaps

The biggest mistake hosts make is confusing these programs with actual insurance. They aren't. Platform protections are essentially guarantee programs, and that distinction changes everything. When you file a claim, it's handled internally by the platform. They act as both judge and jury, deciding if—and how much—they want to pay.

A platform's goal is to smooth over disputes between hosts and guests to keep their marketplace humming. An insurance company's goal is to honor a legal contract and make you financially whole after a covered disaster. These motivations are worlds apart.

When you rely solely on a platform, you’re counting on their goodwill, not the strength of a policy. This can leave you exposed to huge coverage gaps, low payout limits, and a frustrating claims process right when you need help the most.

Key Differences at a Glance

The shortcomings of platform-only protection become crystal clear when you put them side-by-side with a dedicated short term rental insurance policy. The differences are stark, especially when it comes to liability, property damage, and the reliability of getting paid. If you list on multiple sites, it's also crucial to know what each one offers. For example, you can learn more about how VRBO's system works in our detailed 2024 guide.

Savvy owners are catching on. The global market for short-term rental liability insurance has ballooned, hitting between $2.46 billion and $3.18 billion in 2024. This growth isn't just a trend; it's a sign of a maturing industry where hosts understand the need for protection that goes beyond what platforms provide.

The table below breaks down the key differences between what a platform offers and what a private policy delivers.

AirCover for Hosts vs Private STR Insurance

Feature | Platform Protection (e.g., AirCover for Hosts) | Private Short Term Rental Insurance |

|---|---|---|

Type of Coverage | A host guarantee or protection program, not insurance. | A legally binding insurance policy. |

Liability Limits | Capped, often at $1 million. May not cover all types of claims. | Typically higher, customizable limits (e.g., $1M, $2M, or more). |

Property Damage | Numerous exclusions (mold, pests, normal wear and tear). | Comprehensive coverage for the building and its contents. |

Claims Process | Controlled by the platform; decisions are often final. | Formal claims process with an adjuster and legal recourse. |

Loss of Income | Not covered. You lose all revenue if your property is unrentable. | Covered. Reimburses you for lost rental income during repairs. |

Guest Property | Generally not covered if a guest's belongings are stolen or damaged. | Can be included, offering another layer of protection. |

This is precisely where an expert manager makes all the difference. A team like West Coast HomeStays lives and breathes these details. We make sure our San Diego owners aren’t just leaning on platform promises but have a rock-solid policy that truly protects their asset. It’s a critical piece of the hands-off, peace-of-mind management we provide.

Choosing the Right Policy for Your San Diego Rental

Picking the right short term rental insurance isn’t just another item on your to-do list. It’s a critical business decision that protects your entire San Diego investment. The process can feel overwhelming, but if you break it down into a simple roadmap, it’s much more manageable. It all starts with getting brutally honest about what makes your property unique.

Think of it this way: a high-rise condo in the Gaslamp Quarter faces completely different risks than a sprawling beach house in Encinitas with an oceanfront deck and a pool. Your policy has to match your reality. A one-size-fits-all approach is a recipe for disaster when you need that protection the most.

Assess Your Property’s Unique Risks

Before you even start looking at quotes, you need to take a detailed inventory of your property’s specific risk factors. This audit becomes the foundation for figuring out the right coverage levels. Remember, every feature that makes your rental a hit with guests can also be a potential liability.

Start by walking through your property with the mindset of an insurance underwriter. What would they see? Here are a few San Diego-specific examples to get you thinking:

Water Features: Do you have a swimming pool, a hot tub, or direct beach access? These are huge draws for travelers but dramatically increase your liability risk.

Outdoor Amenities: Decks, balconies, fire pits, and rooftop patios are all prime spots for accidents. An oceanfront home in La Jolla with a deck perched on a bluff needs far more robust coverage than a rental tucked away inland.

High-End Contents: Did you invest in premium electronics, designer furniture, or high-end kitchen appliances to attract top-dollar bookings? Your contents coverage needs to be high enough to replace everything if the worst happens.

Local Environment: Coastal properties might face higher risks from storms and saltwater corrosion, while rentals in dense urban neighborhoods could have different security concerns.

Determine Adequate Coverage Limits

Once you’ve cataloged your risks, the next step is to put a real number on them. This is where a lot of hosts get tripped up, often just settling for the bare minimums. Instead, your coverage limits for liability and property should be based on a realistic, worst-case-scenario calculation.

For liability coverage, the industry standard is now $1 million, but if you have significant risks like a pool, it’s smart to consider $2 million or more. For property and contents coverage, create a detailed inventory of your home and everything in it. Calculate the total replacement cost—not the depreciated value—to ensure you could fully rebuild and refurnish after a total loss.

Reading the fine print is non-negotiable. Pay close attention to the policy’s deductibles (what you pay out-of-pocket for a claim) and exclusions (what the policy specifically won't cover). Common exclusions often include things like mold, pest infestations, or certain types of water damage.

Compare Quotes from STR Specialists

Not all insurance companies get the vacation rental market. It’s absolutely crucial to get quotes from insurers who specialize in short term rental insurance. They understand the unique challenges hosts face and build policies designed to fill the gaps left by standard homeowner's insurance.

The wider insurance market is currently dealing with increased competition and new regulations, which can affect premiums. But specialized sectors like STR insurance are adapting by offering products tailored to these specific risks. As you compare quotes, make sure you’re looking at truly comparable policies, not just the final price tag. You can find more insights on how insurers are adapting to market challenges on Deloitte.com.

This is another area where working with a professional manager makes life so much easier. A seasoned team like West Coast HomeStays has deep knowledge of the San Diego market. We know what local regulations require and can point you toward insurers and coverage levels that make sense for your property’s revenue potential, ensuring you aren't underinsured or overpaying. For more details, check out our guide on navigating San Diego's latest short-term rental regulations.

Top Insurance & Management Partners for San Diego Rentals

Choosing the right partners is crucial for maximizing profit and ensuring peace of mind. Here are the top choices for San Diego property owners looking for comprehensive insurance and management solutions.

1. West Coast HomeStays – Hybrid STR/MTR Experts

As San Diego's premier management experts, West Coast HomeStays boosts revenue 20–30% through dynamic pricing, boutique design upgrades, and five-star guest care. Owners enjoy a truly hands-off experience while our hybrid STR + MTR strategy keeps calendars full year-round. Travelers love our amenity-packed, stylish homes near San Diego’s top beaches and attractions.

2. Proper Insurance

A leader in the field, Proper Insurance offers a comprehensive policy designed specifically for short-term rentals, replacing your homeowner's policy entirely. It includes robust liability, property, and loss of income coverage, making it a go-to for serious investors.

3. CBIZ Vacation Rental Insurance

CBIZ provides a commercial insurance policy that can supplement your existing homeowner's policy. It’s known for its flexibility and ability to cover a wide range of property types, from single condos to multi-unit complexes.

🌟 Spotlight on West Coast HomeStays✔ 20–30% revenue boost✔ Hybrid STR + MTR strategy✔ Five-star guest experiences👉 Book a strategy call

If you’re ready for a truly hands-off rental that earns more, West Coast HomeStays is the partner you can trust. We manage everything—from dynamic pricing and design upgrades to five-star guest communication—making sure your asset is not only protected but performing at its absolute peak. For a deeper dive into finding the right partner, check out our guide on how to choose a property management company in San Diego that boosts revenue.

Frequently Asked Questions (FAQ)

When you're thinking about short term rental insurance or professional management, a few questions always come up. Here are some straightforward answers to the things we hear most from San Diego property owners.

What makes West Coast HomeStays different from other managers?

Our difference is a proven, data-driven approach. We combine a hybrid STR + MTR strategy to eliminate vacancies, use dynamic pricing to maximize revenue, and implement design upgrades that command higher rates. The result is a 20-30% average revenue lift and a truly passive income experience for owners, backed by five-star guest service.

Can you handle both short- and mid-term stays?

Yes, this is our specialty. Our hybrid model is designed to keep your calendar full all year. We leverage high-demand seasons for lucrative short-term bookings and pivot to fill shoulder seasons with qualified mid-term tenants like corporate travelers or relocating families. This flexibility ensures consistent, year-round income.

How quickly can my listing be optimized?

Our onboarding is efficient and thorough. We can typically optimize a listing—including professional photography, dynamic pricing setup, and design recommendations—within 2-4 weeks. Our goal is to get your property earning its maximum potential as quickly as possible without cutting any corners on quality.

What amenities do your San Diego homes include?

Our properties are known for being amenity-rich to deliver a boutique hotel experience. Standard amenities include high-speed Wi-Fi, smart TVs, fully-equipped kitchens, premium linens, and keyless entry. Depending on the property, we also highlight features like pools, hot tubs, dedicated workspaces, and family-friendly items to attract the ideal guests.

Do you help with design upgrades to boost nightly rates?

Absolutely. This is a core part of our value. We provide expert interior design consultations to create stylish, comfortable spaces that photograph beautifully and earn five-star reviews. These strategic upgrades are proven to increase nightly rates and occupancy, directly boosting your bottom line.

If you’re ready for truly hands-off, higher-earning rentals in San Diego, West Coast HomeStays is the partner to trust. Book a no-obligation strategy call today and let's transform your property's performance together.

Comments